A quick update on Core Molding Technology (CMT), which announced a new business award with Volvo last week. CMT was written up on the blog almost one year ago – check out the original post.

The major details from the press release are included below (emphasis is mine):

“Core expects the new business to generate annual revenues of approximately $26-$30 million and anticipates revenues beginning late in the second quarter and ramping up by the fourth quarter of 2013. Planning and staffing activities are underway as the Company is evaluating facilities to produce these heavy duty truck hoods, roofs and other molded parts for Volvo. This new business is expected to employ up to 140 additional people. Core plans to make an additional capital investment of approximately $12.5 million throughout 2013 and 2014 for equipment and infrastructure to support this and other business.”

The market responded positively, sending the stock price up more than 20% over the past two days. With $168m in TTM sales, $28m in incremental revenue (at the midpoint of the expected range) represents a 16.7% increase. The new business will reach full production by the end of the fiscal year.

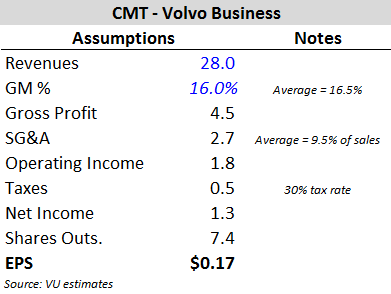

While specific profitability information is not provided, estimates can be made based on CMT’s long-term business metrics:

Looking at the increase in hiring, $28m in incremental revenue with 140 new workers translates into sales/employee of $200k for this new business vs. $110k sales/employee for the company as a whole. This makes sense (few if any admin personnel will be need to be hired at HQ for example), and should provide some leverage on the SG&A line.

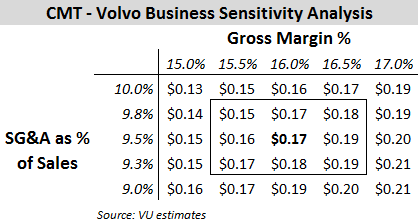

However, the biggest risk is that management sacrificed pricing in order to win such a significant award, which would impact gross margins. A sensitivity analysis is included below:

If the long-tern economics hold true, it seems reasonable to assume that the new business will add $0.15-$0.19 EPS. At a 10x multiple on the mid-point, this Volvo award is worth $1.66/share in value to CMT, close to the $1.59/share added to the stock price in the last two days.

On the investment side, the company is planning to spend $12.5m in capex to “support this and other business.” If 90% of the planned capex is for Volvo, it would equal capex/share of $1.52 and an acceptable ROI of 11.3%.

Other Thoughts

Prior to this announcement, the stock had struggled since May (hitting a low of $6.35 in January).

One part of the original thesis was that record backlog would boost the top line. While Q1 and Q2 sales were up 54% and 26% YoY respectively, sales growth stalled in the second half of the year (Q3 was flat).

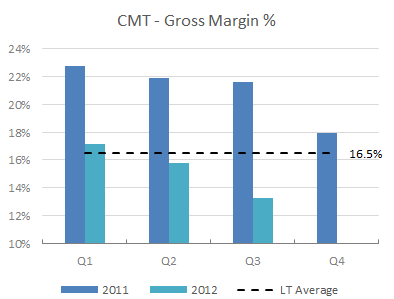

Most important, profitability did not follow the sales growth – gross margin fell materially due to a combination of production inefficiencies, change in product mix to lower margin products, increased tooling sales, and start-up costs for the Kentucky subsidiary:

A major contributor to the margin compression was costs for the Kentucky subsidiary, a short-lived and disappointing initiative. The facility was created in July 2011 to diversify away from trucking-related subsidiaries, with an expectation of $5-8m in annual revenue at full production.

However, the facility’s major customer reversed course suddenly, terminating the relationship in June 2012. The facility was closed in October 2012. This failed project impacted margins throughout the year, in addition to consuming $1.2m in leasehold improvements.

With the facility now closed, this drag on earnings and management attention will go away and gross margins should revert to the long-term average (pending pricing terms on the Volvo deal of course).

Conclusion

Ultimately, the Volvo business helps mitigate one of the biggest risks associated with CMT: customer concentration. Sales to Navistar and PACCAR represented 80% of sales in 2011, especially troubling considering the difficulties at Navistar.

Therefore, the addition of a 3rd major customer is great news for the long-term stability of the business.

The trucking cycle continues to improve (225k units in 2012, up from 197k in 2011; 210-240k expected for 2013), as the age of the fleet remains near all-time highs.

Despite the operational missteps, CMT will likely report record results in 2012 and is still priced like a no-growth business despite long-run evidence to the contrary.

Disclosure

Long CMT

[…] Core Molding Technologies, CMT – Approximately 5% of portfolio. First article I wrote about them can be viewed here. As of today up 27% since buying into them in August of 2012. The company has won multiple awards in recent months for being an excellent supplier and has also added significant additional business with Volvo. […]